Steve Katz, Editor09.07.16

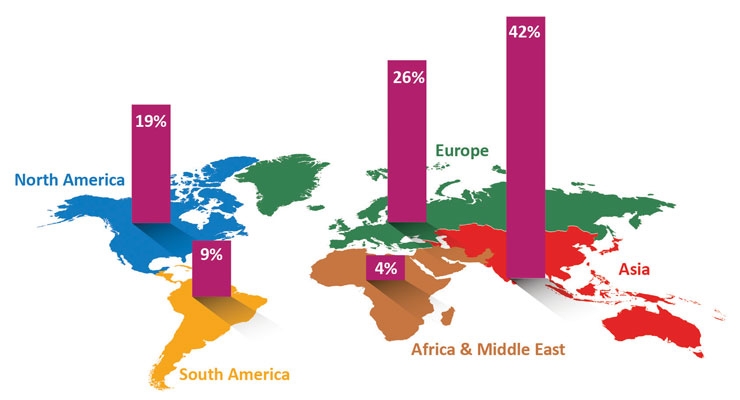

North America, which is made up of the United States, Canada and Mexico, represents 19% of global demand for labels. AWA Alexander Watson Associates is a global business-to-business market research, publishing, events and advisory services company with a unique focus on the specialty packaging, coating and converting industries. Based in Amsterdam, the firm has offices in both Chicago and Thailand. According to AWA, North America is currently the third-largest region in terms of label demand, with Asia taking the lion’s share at 42%.

Overall, the North American label market grew 1.5-2% in 2015. Across the region, AWA reports, glue-applied labels grew at just 0.4%, though the segment retains a 30% share of the market. Higher growth rates were enjoyed by the other mainstream labeling technologies – sleeving of all kinds, 2.9%, pressure sensitive (PS) labels, 2.5%, and in-mold labels, 2.4%. AWA notes that in-mold labeling looks set to enjoy a CAGR of 2.7% in the years to 2020 – the highest forecast growth of all the main technologies, albeit from a low base. “The IML-IM formats continue to make particularly strong gains in the region and enjoyed a 7% volume improvement in 2015,” says Corey Reardon, president and CEO at AWA.

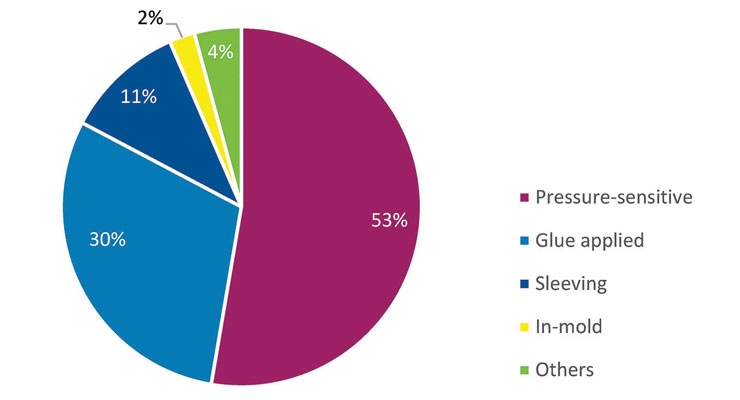

The majority of the current North American label demand, which sits at 53%, is in pressure sensitive labels. AWA forecasts that the PS label market will continue to enjoy over 2% annual growth to 2020, offering a wide-ranging “package” of benefits for the brand owner that can include security features within the substrate, serialization, printed electronics, QR codes and personalization – with the use of multiple converting technologies, both analog and digital – that can accommodate both long and short print runs.

The newer technologies – sleeving of all kinds and in-mold labeling – command current market shares of just 11% and 2% respectively, AWA data shows. “Sleeving, particularly heat-shrink TD sleeves for beverage labeling, will continue to grow at a healthy rate, but it may now be in sight of its demand zenith as more recent innovations, such as direct-to-container print and flexible packaging, attract brand owner attention,” Reardon says.

Shorter print runs across the board are characterizing the product identification market, as product multi-versioning and brand owners’ demand for just-in-time delivery are challenging converters. Concludes Reardon, “Other challenges within the region are factors within the packaging market as a whole – particularly in the recycling arena, with recycling of labeled PET containers a particular focus at present across the value chain.”

Moving forward

LPC, Inc. is another great resource for companies at every level of the labels and packaging supply chain. With headquarters in Austin, TX, USA, and London, England, LPC works with consumer product companies, printers and converters, and equipment and consumable goods suppliers.

The breadth of LPC’s research includes the global packaging market, and the firm has significant expertise of the North American label industry. According to LPC managing director Jennifer Dochstader, the North American label printing industry is growing, and all labeling formats – with the exception of glue-applied – are projected to grow at or above GDP over the next five years.

Digital printing is top of mind for many label converters today. LPC projects that the North American market for digital labels will continue to grow at double-digit rates. “We estimate that just over 9% of the North American market is currently printed digitally,” Dochstader says.

LPC notes that in North America and Canada, there are about 2,000 label converters with annual revenues greater than $1 million. According to LPC data, in 2015, 218 new label presses (brand new, not used) were sold into the US and Canada. This figure includes both conventional and digital presses, and as far as digital goes, it accounts for production class machinery only, excluding label printers of the tabletop variety.

“2015 was a good year for the industry,” states Dochstader. “In North America, we saw growth across the labeling subsectors; continued migration to film from paper labelstocks drove prime label growth in the food and beverage sectors. The growing online retail sector fueled the growth of non-prime VIP applications, including direct thermal, thermal transfer and EDP labels. For the different types of research LPC does, we speak with label converters nearly every day, and companies are reporting growth in other non-prime areas as well, including medical device, consumer durables, automotive and industrial labeling.”

She adds, “Converters’ average flexo press downtime rates hover around 30%, and when converters are asked what the leading causes are of idle presses, the majority of companies cite short run sizes. Presses are down due to more and more job make-readies and changeovers.”

LPC recently carried out an extensive multi-client market research endeavor in the digital press space and estimates that more than 130 digital production presses will be sold into the US and Canada in 2016. “These presses will be electrophotography presses, inkjet presses and the new hybrid systems we saw introduced at Labelexpo in Brussels last year. The advancements in digital press technology will lead to digital capturing more and more conventional market share,” Dochstader explains. “Something else we are all paying close attention to is the reality of brand owners and contract packagers bringing digital in-house and switching from outsourcing printed labels to producing them internally. We are seeing these vertically integrated operations printing everything from coffee bag labels, to beef jerky labels, to nutraceutical labels to labels for the vaping/e-cigarette industry. These brands once sourced labels from converters; however are now meeting some or all of their label production needs in-house.”

In addition to digital printing in general, Dochstader predicts that the “hot” sectors in the coming years will be extended text/extended content applications, industrial labels, the medical device sector, sleeves, and more label converters producing flexible packaging applications on their narrow web presses.

“Conventional label press manufacturers have raised the bar, and today’s flexo presses are capable of printing and converting traditional unsupported flexible packaging films on an inline press,” Dochstader adds. “The pace of change in our industry hasn’t slowed down. It’s certainly an interesting time to be a North American label converter.”

For more information about LPC, visit www.lpcprint.com.

Label legislation and the need for accuracy

Market-wise, the food and beverage sectors together make up 56% of total value of the North American label printing industry, with food accounting for 27% and beverage taking up 29% of market share. Next up in North America, according to LPC, is health and beauty/personal care (7%) and pharmaceutical, household chemicals and transport/logistics each with a 6% share of the market. Rounding out the end use sectors is consumer durables and industrial chemicals at 5%, automotive 3%, retail 2%, and “other” with 4%.

In the US, legislation regarding label content requirements have consistently been making headlines. In fact, on July 29, 2016, President Obama signed into law S. 764, which overturns Vermont’s GMO label law and establishes a US national standard for the GMO (genetically modified organism) labeling of products. The legislation is intended to avoid a mix of state-specific GMO label laws, and will preempt state-level GMO labeling laws. For example, Vermont’s mandatory GMO labeling law, which took effect on July 1, will be preempted, as will laws in Connecticut and Maine that that have not yet taken effect. These state laws require labels for food products sold in their respective states to display whether the food was produced entirely or partially with genetic engineering. The GMO issue is just one example. Labeling laws change regularly, especially those involving health and nutrition. As such, label accuracy plays a critical role in virtually every industry, but particularly in the food, beverage, pharmaceutical and medical spaces.

With accuracy being a paramount concern for brand owners, also becoming more important are fully-integrated bar code label software solutions that grow with businesses over time while increasing label accuracy. “The software itself reduces the room for human error throughout the labeling process by eliminating manual processes, providing intuitive label templates and offering the ability to fully-integrate with ERP systems,” says David Kane, labeling software specialist and TEKLNX’s Label Design product manager. For one TEKLYNX manufacturing customer, Kane says, integrating bar code labeling software into its ERP system led to a 50% reduction in labeling errors and an equal decrease in costly customer returns.

The complexity of food traceability, labeling and recall planning and management led to the FDA’s Food Safety Modernization Act (FSMA), its most comprehensive food safety reform in over 70 years. A testament to the growing concern for the safety of the food supply and the need for change, Kane says the FSMA is a major step toward shifting the focus from how food manufacturers, suppliers and retailers respond to food contamination to how they prevent food contamination – requiring food companies to take a more proactive approach to food safety management.

Says Kane, “Proactive management requires accurate labeling because it’s often the very thing that can avoid a recall from happening in the first place. Should a recall be initiated, labeling software allows food manufacturers to quickly identify, locate and remove affected products. Bar code labeling software solutions also prove invaluable on the back end of a recall because they enable a full view into labeling history – reducing the amount of time required to locate the products and expedite the recall. In fact, for a leading food manufacturer, the implementation of TEKLYNX Central not only made the label printing process timelier and more accurate, but also put an end to complete production shutdowns as a result of a labeling inaccuracy.”

Like the food industry, manufacturers of medical devices face fierce global competition and a myriad of strict regulatory requirements. “Few industries are as complex and regulated as medical devices,” Kane says. “Standards for quality, safety and procedural accuracy are exceedingly high – as are the stakes – and failure to meet these standards can have profound consequences. This means a small action, like an incorrect key stroke, could lead to a time-consuming corrective action process; thus, decreasing productivity. So, much like food manufacturers, the key to success in the labeling of medical devices is proactivity.

“A testament to the industry’s labeling complexities, leading medical device packaging and outsourcing solutions provider Quality Tech Services (QTS) was faced with incorporating ISO symbols and adhering to a variety of FDA 21 CFR Part 11 criteria for electronic signatures while meeting new Unique Device Identification (UDI) compliance deadlines. Intent upon meeting compliances and proactively preventing issues, the QTS team implemented TEKLYNX Central CFR, an enterprise-level bar code labeling software solution,” Kane says. “After implementation, QTS soon realized its benefits of label accuracy extended beyond meeting compliances and regulations. By fully-integrating the labeling software with its existing ERP system, QTS significantly increased label accuracy by eliminating 100% of the need for manual entries at time of print.”

Overall, the North American label market grew 1.5-2% in 2015. Across the region, AWA reports, glue-applied labels grew at just 0.4%, though the segment retains a 30% share of the market. Higher growth rates were enjoyed by the other mainstream labeling technologies – sleeving of all kinds, 2.9%, pressure sensitive (PS) labels, 2.5%, and in-mold labels, 2.4%. AWA notes that in-mold labeling looks set to enjoy a CAGR of 2.7% in the years to 2020 – the highest forecast growth of all the main technologies, albeit from a low base. “The IML-IM formats continue to make particularly strong gains in the region and enjoyed a 7% volume improvement in 2015,” says Corey Reardon, president and CEO at AWA.

The majority of the current North American label demand, which sits at 53%, is in pressure sensitive labels. AWA forecasts that the PS label market will continue to enjoy over 2% annual growth to 2020, offering a wide-ranging “package” of benefits for the brand owner that can include security features within the substrate, serialization, printed electronics, QR codes and personalization – with the use of multiple converting technologies, both analog and digital – that can accommodate both long and short print runs.

The newer technologies – sleeving of all kinds and in-mold labeling – command current market shares of just 11% and 2% respectively, AWA data shows. “Sleeving, particularly heat-shrink TD sleeves for beverage labeling, will continue to grow at a healthy rate, but it may now be in sight of its demand zenith as more recent innovations, such as direct-to-container print and flexible packaging, attract brand owner attention,” Reardon says.

Shorter print runs across the board are characterizing the product identification market, as product multi-versioning and brand owners’ demand for just-in-time delivery are challenging converters. Concludes Reardon, “Other challenges within the region are factors within the packaging market as a whole – particularly in the recycling arena, with recycling of labeled PET containers a particular focus at present across the value chain.”

Moving forward

LPC, Inc. is another great resource for companies at every level of the labels and packaging supply chain. With headquarters in Austin, TX, USA, and London, England, LPC works with consumer product companies, printers and converters, and equipment and consumable goods suppliers.

The breadth of LPC’s research includes the global packaging market, and the firm has significant expertise of the North American label industry. According to LPC managing director Jennifer Dochstader, the North American label printing industry is growing, and all labeling formats – with the exception of glue-applied – are projected to grow at or above GDP over the next five years.

Digital printing is top of mind for many label converters today. LPC projects that the North American market for digital labels will continue to grow at double-digit rates. “We estimate that just over 9% of the North American market is currently printed digitally,” Dochstader says.

LPC notes that in North America and Canada, there are about 2,000 label converters with annual revenues greater than $1 million. According to LPC data, in 2015, 218 new label presses (brand new, not used) were sold into the US and Canada. This figure includes both conventional and digital presses, and as far as digital goes, it accounts for production class machinery only, excluding label printers of the tabletop variety.

“2015 was a good year for the industry,” states Dochstader. “In North America, we saw growth across the labeling subsectors; continued migration to film from paper labelstocks drove prime label growth in the food and beverage sectors. The growing online retail sector fueled the growth of non-prime VIP applications, including direct thermal, thermal transfer and EDP labels. For the different types of research LPC does, we speak with label converters nearly every day, and companies are reporting growth in other non-prime areas as well, including medical device, consumer durables, automotive and industrial labeling.”

She adds, “Converters’ average flexo press downtime rates hover around 30%, and when converters are asked what the leading causes are of idle presses, the majority of companies cite short run sizes. Presses are down due to more and more job make-readies and changeovers.”

LPC recently carried out an extensive multi-client market research endeavor in the digital press space and estimates that more than 130 digital production presses will be sold into the US and Canada in 2016. “These presses will be electrophotography presses, inkjet presses and the new hybrid systems we saw introduced at Labelexpo in Brussels last year. The advancements in digital press technology will lead to digital capturing more and more conventional market share,” Dochstader explains. “Something else we are all paying close attention to is the reality of brand owners and contract packagers bringing digital in-house and switching from outsourcing printed labels to producing them internally. We are seeing these vertically integrated operations printing everything from coffee bag labels, to beef jerky labels, to nutraceutical labels to labels for the vaping/e-cigarette industry. These brands once sourced labels from converters; however are now meeting some or all of their label production needs in-house.”

In addition to digital printing in general, Dochstader predicts that the “hot” sectors in the coming years will be extended text/extended content applications, industrial labels, the medical device sector, sleeves, and more label converters producing flexible packaging applications on their narrow web presses.

“Conventional label press manufacturers have raised the bar, and today’s flexo presses are capable of printing and converting traditional unsupported flexible packaging films on an inline press,” Dochstader adds. “The pace of change in our industry hasn’t slowed down. It’s certainly an interesting time to be a North American label converter.”

For more information about LPC, visit www.lpcprint.com.

Label legislation and the need for accuracy

Market-wise, the food and beverage sectors together make up 56% of total value of the North American label printing industry, with food accounting for 27% and beverage taking up 29% of market share. Next up in North America, according to LPC, is health and beauty/personal care (7%) and pharmaceutical, household chemicals and transport/logistics each with a 6% share of the market. Rounding out the end use sectors is consumer durables and industrial chemicals at 5%, automotive 3%, retail 2%, and “other” with 4%.

In the US, legislation regarding label content requirements have consistently been making headlines. In fact, on July 29, 2016, President Obama signed into law S. 764, which overturns Vermont’s GMO label law and establishes a US national standard for the GMO (genetically modified organism) labeling of products. The legislation is intended to avoid a mix of state-specific GMO label laws, and will preempt state-level GMO labeling laws. For example, Vermont’s mandatory GMO labeling law, which took effect on July 1, will be preempted, as will laws in Connecticut and Maine that that have not yet taken effect. These state laws require labels for food products sold in their respective states to display whether the food was produced entirely or partially with genetic engineering. The GMO issue is just one example. Labeling laws change regularly, especially those involving health and nutrition. As such, label accuracy plays a critical role in virtually every industry, but particularly in the food, beverage, pharmaceutical and medical spaces.

With accuracy being a paramount concern for brand owners, also becoming more important are fully-integrated bar code label software solutions that grow with businesses over time while increasing label accuracy. “The software itself reduces the room for human error throughout the labeling process by eliminating manual processes, providing intuitive label templates and offering the ability to fully-integrate with ERP systems,” says David Kane, labeling software specialist and TEKLNX’s Label Design product manager. For one TEKLYNX manufacturing customer, Kane says, integrating bar code labeling software into its ERP system led to a 50% reduction in labeling errors and an equal decrease in costly customer returns.

The complexity of food traceability, labeling and recall planning and management led to the FDA’s Food Safety Modernization Act (FSMA), its most comprehensive food safety reform in over 70 years. A testament to the growing concern for the safety of the food supply and the need for change, Kane says the FSMA is a major step toward shifting the focus from how food manufacturers, suppliers and retailers respond to food contamination to how they prevent food contamination – requiring food companies to take a more proactive approach to food safety management.

Says Kane, “Proactive management requires accurate labeling because it’s often the very thing that can avoid a recall from happening in the first place. Should a recall be initiated, labeling software allows food manufacturers to quickly identify, locate and remove affected products. Bar code labeling software solutions also prove invaluable on the back end of a recall because they enable a full view into labeling history – reducing the amount of time required to locate the products and expedite the recall. In fact, for a leading food manufacturer, the implementation of TEKLYNX Central not only made the label printing process timelier and more accurate, but also put an end to complete production shutdowns as a result of a labeling inaccuracy.”

Like the food industry, manufacturers of medical devices face fierce global competition and a myriad of strict regulatory requirements. “Few industries are as complex and regulated as medical devices,” Kane says. “Standards for quality, safety and procedural accuracy are exceedingly high – as are the stakes – and failure to meet these standards can have profound consequences. This means a small action, like an incorrect key stroke, could lead to a time-consuming corrective action process; thus, decreasing productivity. So, much like food manufacturers, the key to success in the labeling of medical devices is proactivity.

“A testament to the industry’s labeling complexities, leading medical device packaging and outsourcing solutions provider Quality Tech Services (QTS) was faced with incorporating ISO symbols and adhering to a variety of FDA 21 CFR Part 11 criteria for electronic signatures while meeting new Unique Device Identification (UDI) compliance deadlines. Intent upon meeting compliances and proactively preventing issues, the QTS team implemented TEKLYNX Central CFR, an enterprise-level bar code labeling software solution,” Kane says. “After implementation, QTS soon realized its benefits of label accuracy extended beyond meeting compliances and regulations. By fully-integrating the labeling software with its existing ERP system, QTS significantly increased label accuracy by eliminating 100% of the need for manual entries at time of print.”